Fill out the form below and our team will be with you in no time.

Need help?

Start conversation

Start conversationRead mode

This years EMARKETER’s 2026 D2C report presented one interesting number, thats gonna have massive impact in marketing decisions in the following years.

That number is the share of total retail ecommerce that D2C brands hold in 2026. It took D2C about a decade to climb to 19%. EMARKETER projects it will sit there, flat, through 2028.

After ten years of being framed as the future of commerce, D2C just hit a wall.

D2C was the model that was supposed to fix everything wrong with marketing:

It was supposed to compound. Instead it starting to stop.

And here is the part that should matter to every CMO, not just the D2C ones.

The reasons it stalled are the same reasons I have watched my clients struggle with their marketing channels for years.

Apple’s App Tracking Transparency in 2021 made targeted ads dramatically more expensive overnight. Customer acquisition cost went up and didn’t come back down. Then Amazon and the marketplaces ate share, and D2C brands ended up competing on exactly the shelves they were supposed to bypass.

Then VC money stopped subsidising growth-at-all-costs and everyone had to suddenly pay for acquisition out of revenue instead of out of someone else’s patience.

On top of all that, AI search is rewriting how people find products in the first place.

EMARKETER reports a 1200% jump in AI-driven traffic to brand sites between mid-2024 and early 2025.

The buying journey is moving from search engines to chat interfaces, and most marketing teams we talk to haven’t fully adopted that in yet.

The combined picture is uncomfortable: the channels brands have been renting for the last decade are getting more expensive, less trusted, and less effective every quarter.

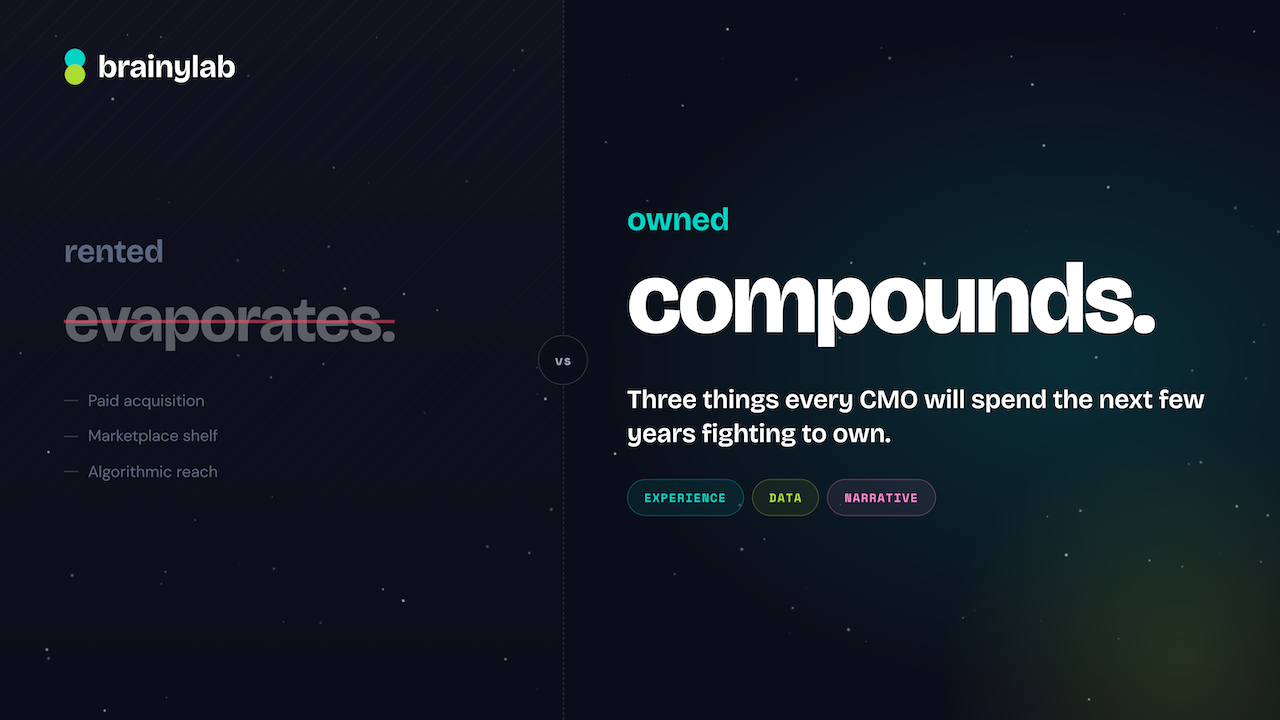

There is one line in EMARKETER’s report that I think every CMO should put on the wall.

It is becoming less about volume share and more about Control: of Experience, Data, and Narrative.”

Three controls.

And this applies to every brand we have ever worked with: Telco, Pharma, Insurance, Retail, Automotive, FMCG. Every one of them is fighting for those three things. And every channel they have been renting to fight for them is getting weaker at the same time it is getting more expensive.

🎁 Experience

Own the moment when a customer interacts with your brand.

The thing they see, click, play, or read. If it lives on your channel, you decide how it looks, how it works, and what comes next. If it lives on Meta or Google or a marketplace, you don't.

📊 Data

Own who that customer is, what they care about, and how they behave.

First-party data: names, preferences, behaviour, intent. Collect them with clear stated permission and store yourself. The kind of data that doesn't disappear when Apple updates iOS or Google deprecates a cookie.

❤️ Narrative

Own the story your brand tells.

Why your brand exists, what it stands for, what it offers, in your words, on your surfaces, without a publisher or a platform editing it down.

First thing to keep in mind is that owned audience compounds. Rented audience evaporates the moment you stop paying.

So the question is How to steer away from that? How to build owned audience that wants to communicate and interact with your brand?

Sure, there are some local and size constraints - for instance, Ramp (a b2b financial company) is building their own media infrastructure. Not an AI blog or very advanced content strategy. An actual media house to attract their Ideal Customer Personas (ICPs) to their domain. With heavy AI layer on top of it, but with human writers and deep deep stories and reporting.

Most of the brands we work with are not going to publish trade journalism on their own domain. A car company is not going to start running a content studio. An insurer is not going to build a meme account (or should they?) A telecom is not going to launch a podcast network.

But their customers do scroll. They tap. They compare. They quiz themselves on which service fits their family. They configure a product they are considering. They check whether they qualify for a benefit. They play, sometimes for thirty seconds, sometimes for ten minutes.

That is where the same three controls apply — through interactive experiences instead of editorial.

A quiz, a calculator, a configurator, a simulation, a branded game — done well, each one is a piece of owned media that does three jobs at once. It earns attention through the experience itself instead of buying it through paid distribution. It collects first-party data as a byproduct of the interaction, not as a friction-y form bolted on at the end. And it lets the brand control the narrative end-to-end, frame by frame, with no platform sitting in the middle.

We've been working with brands on these kinds of experiences for the last 5 years. Different industries, goals, and mechanics. Same three controls.

A1 Spletne brihte: A gamified learning platform for kids, parents, and teachers. People come back, on their own, through newsletter reminders and with way less paid retargeting. Average time on platform sits above 12 minutes.

Citroen edutianment strategy: Asynchronous interactive experiences that turn their existing website traffic into segmented, opted-in subscribers. No additional media spend. Just an interactive experience that gave people a reason to tell Citroen who they are and what they were looking for.

Argeta: Argeta truly values quality and emotional connections with people. On any given channel. Digital tools, helpers, calculators, generators they have built to engage and give unique online experience is amazing!

Different audiences, different mechanics, different moments in the year. Every tool earns attention, captures first-party data, and segments the audience a little more precisely than the last one. That is what owned media looks like as a strategy. The outcomes of Argeta (present on 20+ markets and leader in various consumer categories) are quite obvious and seen year over year.

Sava Insurance: Insurance is one of the hardest categories to make people care about. Nobody wakes up wanting to think about their policy.

Sava decided to fight that by building tools their customers actually want to engage with. Sava Ava, a quiz-based learning tool, a gamified family book, internal educational tools ... and all of that on their own channels and with rich customer data to build upon.

Different industries. Same underlying pattern. Build something the customer actually wants to interact with. Capture what they tell you. Control the experience end to end.

And this brings us to the final question.

You are probably already seeing that AI is about to make the brands with good data unrecognisably better than the brands without it.

Every personalisation tool we are building right now, recommendation engines, AI agents, mass-personalisation tools, dynamic content generators, run on the same fuel. Customer data or their interaction in real time.

But if you have the data to start with, you're already in the advantage.

The cleaner, the richer, the more consented, the better the output. A generic AI agent is a chatbot. An AI agent trained on the actual preferences, behaviour, and purchase history of your real customers is a competitive moat.

The data you collect today is what your AI uses three months from now. If you start now, by 2028 you have an asset compounding quietly in the background. If you don't, you spend 2028 trying to buy your way back into a race you forgot was happening.

Data given freely, with clear value in exchange, is data that actually means something. Data scraped or assumed is data your AI will hallucinate against.

Garbage in, confidently wrong out.

The brands that collect quality data with permission are the ones whose AI will actually work. Everyone else will be running expensive demos.

If you are trying to figure out what this looks like for your brand, what experience fit your ideal target audiences, what data it should capture, what those three controls mean in your context ... that is most of what we do.

Drop us a message and reserve your free discovery call.